A Leveraged Buyout (LBO) is one of the most iconic transactions in finance: acquiring a company through a combination of debt and equity. The purpose of this page is to walk through a complete LBO model — from base assumptions to IRR.

Starting Assumptions

These are the starting assumptions given (no calculations here):

- Revenues (LTM): 100 M$

- Annual Revenue Growth: 10% (constant for 5 years)

- EBITDA (LTM): 50 M$

- EBITDA Margin: constant

- D&A + Capex: 5% of annual revenues

- NWC: unchanged

- Tax Rate: 25%

- Entry Multiple: 10x EBITDA

- Exit Multiple: 10x EBITDA after 5 years

- Projection Period: 5 years

- Initial Leverage: 6x EBITDA

- Debt Interest Rate: 8%

- No capital amortization until maturity

TEV & Capital Structure

Now we start calculating the purchase TEV and the initial capital structure (Debt & Equity).

- EBITDA LTM = 50

- Entry Multiple = 10x

- TEV_in = 50 × 10 = 500

- Initial Leverage = 6 × EBITDA ⇒ Debt = 6 × 50 = 300

- Equity = 500 − 300 = 200

Result: TEV_in = 500; Initial Debt = 300 (60%); Equity Sponsor = 200 (40%).

Interest Expense on Debt

Debt is not amortized during the 5-year period, so interest is flat each year.

- Total Debt = 300

- Interest Rate = 8%

- Annual Interest Expense = 300 × 8% = 24

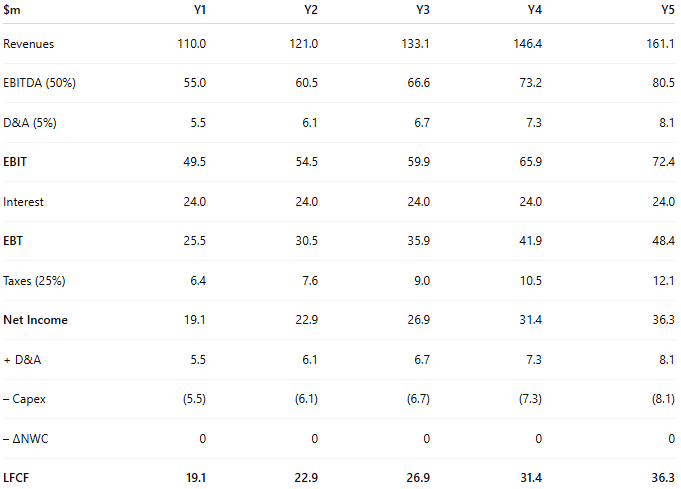

Projection over 5 Years

We project P&L down to (levered) free cash flow over five years.

Exit TEV & Returns

Step 1 — Exit TEV

- EBITDA Y5 = 80.5

- Exit Multiple = 10x

- TEV_out = 80.5 × 10 = 805

Step 2 — Exit Equity Value

- TEV_out = 805

- Net Debt = 300

- Equity Exit Value = 805 − 300 = 505

Step 3 — Returns

- Invested Equity = 200

- Exit Equity = 505

- MoM = 505 / 200 = 2.53x

I estimated the IRR by intuition: ~20% for ~2.5x in 5 years (rule-of-thumb: 2x in 5y ≈ 15%; 3x in 5y ≈ 25%).